![Daniël Klijn [LittleDean]](http://www.littledean.nl/wp-content/uploads/2018/10/cropped-Littledean-LONG-wit-1-1-1.png)

Multi-product break-even analysis Business Economics Vocab, Definition, Explanations Fiveable

In the dynamic world of business, understanding the break-even point is crucial for making informed decisions regarding pricing, production, and profitability. While calculating the break-even point for a single product is relatively straightforward, the process becomes more complex when dealing with multiple products. This essay explores the methodology for determining tax deadline is april 15, 2021 for 2020 taxes tax day 2021 the break-even point when multiple products are being sold and provides a hypothetical example to illustrate the concepts. For these products, with a sales mix of 90%/10%, the weighted average contribution for every unit sold is 2.20 as shown in the diagram below. If the sales mix is different from our estimate, the break even point will not be the same.

Plan Projections

In this article, we would explain the procedure of calculating break-even point of a multi-product company. So we need to break up the 180 units into the 3 different products using our mix of 60%. Management might want to know what the volume of sales must be in order to achieve a target profit. Using a forecasted or estimated contribution margin income statement, we can verify that the quantities listed will place West Brothers at break-even. For Multi-product margin of safety, the break-even point can be compared to the budgeted activity level using batches, units or revenue. Suppose for example, our business has the same operating expenses of 4,500, but this time is has two product lines.

Step 6: Calculate the Total Variable Expense

Notice that the composite contribution margin is based on the number of units of each item that is included in the composite item. Calculate the weighted average contribution margin by considering the proportion of each product’s sales to total sales. In the YouTube video below, I use Excel to find the break-even with multiple products. I demonstrate the array function, use conditional formatting, and work with absolute reference to find the weighted average contribution margin per unit.

Business Economics

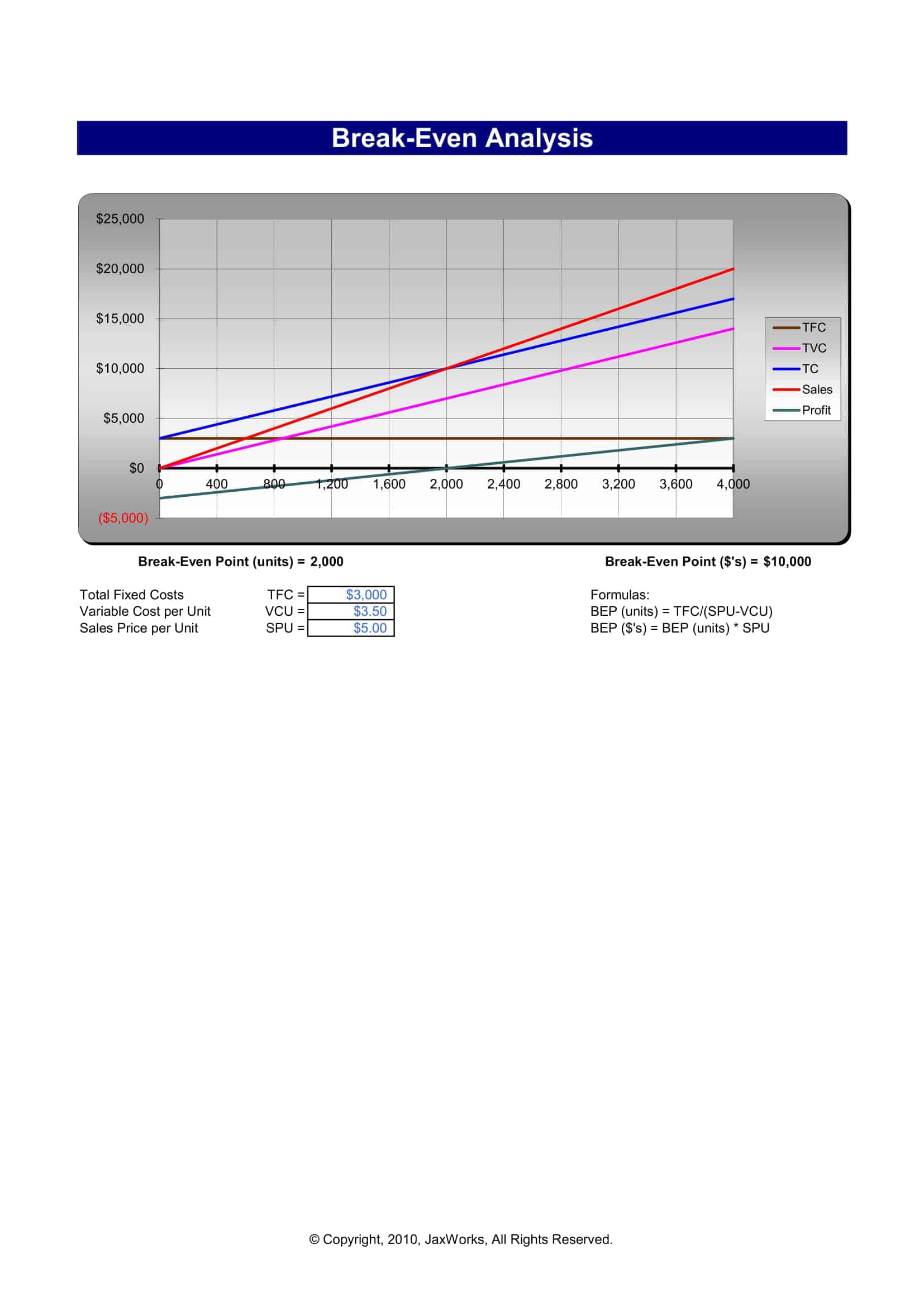

At this point, the total costs of the business are covered by the total revenue the business generates. Another way of putting this is that the contribution earned by the business is just enough to cover the fixed costs. This chart plots a single line depicting the profit or loss at each level of activity. The procedure of computing break-even point of a multi-product company is a little more complicated than that of a single product company.

Let’s Get Social

Sales mix is important to business owners and managers because they seek to have a mix that maximizes profit, since not all products have the same profit margin. Companies can maximize their profits if they are able to achieve a sales mix that is heavy with high-margin products, goods, or services. If a company focuses on a sales mix heavy with low-margin items, overall company profitability will often suffer. For computing break-even point of a company with two or more products, we must know the sales percentage of individual products in the total sales mix.

How to calculate your break-even point: A guide for ecommerce businesses

Calculating the the number of units which need to be sold for the business to reach break even is relatively straight forward when a business sells only one product. Costs that do not change with the level of production or sales, such as rent and salaries, essential for calculating the break-even point. The weighted average CM may also be computed by dividing the total CM by the total sales. In this formula, I have subtracted the fixed expense from the contribution margin. You will get the unit for all the products that should be sold to cover the costs. In this formula, I multiplied the unit variable expense by the expected sale for each product and used the SUM function to add them.

- Fixed costs remain constant regardless of the volume of products sold (e.g., rent, salaries).

- Let’s look at an additional example and see how we find the break-even point for this weighted average basket.

- In this formula, I have multiplied the unit sale by the expected sale for each product.

- Calculate the weighted average contribution margin by considering the proportion of each product’s sales to total sales.

- So we need to break up the 180 units into the 3 different products using our mix of 60%.

Our comprehensive guide covers everything you need to know about calculating your break-even point as an ecommerce business owner.

The following underlying assumptions will limit the precision and reliability of a given cost-volume-profit analysis. The company must produce and sell 800 units of Product A, 1,600 units of Product B, and 4,000 units of Product C in order to break-even. If we know we need $125,000 in sales to break even but the sales mix is different from what we budgeted, the numbers will appear quite different (as you should have noticed in the video). In a multi-product environment, calculating the break-even point requires careful consideration of the individual cost structures, selling prices, and sales volumes for each product.

The only difference is that the denominator is the weighted average contribution per unit (for break-even point in units) or weighted average contribution to sales (C/S) ratio (for Break-even Revenue). The necessary contribution to earn the target profit is the target profit plus the fixed costs. The activity level required to achieve the necessary contribution may be found using contribution per unit, contribution per batch or the CS ratio. Although you are likely to usecost-volume-profit analysis for a single product, you will morefrequently use it in multi-product situations.